The plot thickens. Gold, in US dollar terms, tagged all-time historic highs last week, registering a monthly close on the charts that has a universe of traders looking in.

Some say prices are overheating. Some believe the $2000 level will generate an impulsive round of profit-taking. Some, including me, think calling the short-term moves in the early stages of a bull market cycle is a mug’s game. But if pressed, I don’t believe $2k will halt this phase of the rally.

Here’s a (one hour) intra-day chart showing off an Ascending Triangle, with a rising (support) trendline for those technically inclined:

We’re now at a stage where picking high-quality stocks, those that haven’t ripped higher in recent weeks/months is becoming increasingly difficult.

I’m looking at roughly a half-dozen stocks right now in an effort to grow the Highballer shortlist. The criteria I layout for a shortlist candidate—competent management, mining-friendly jurisdiction, prospective geological setting, meaningful ounces-in-the-ground, tight market cap—rarely line up, collectively speaking. Even one single kink, say a blown-out share structure, can destroy the order.

It’s probably accurate to state that in this current lofty environment—these early innings of what I expect will evolve into an epic (multi-year) bull market run—we now need to pay-up for high-quality plays.

Fair enough, but there’s still value out there. You just need to dig.

And it helps to collaborate with those tracking the same quarry—those with the same values, experience, and obsession for the hunt. More on this further down the page.

What I’m currently looking for at this stage of the bull cycle is an advanced stage development play with a solid resource base and significant exploration upside. Tough duty, huh?

If a company I like lacks a 43-10 resource, an eight-figure JV with a deep-pocketed Sr. mining behemoth will do. Again, more on this further down the page.

With some advanced stage development plays—those whose current primary focus is development, permitting, and pre-construction activities—there’s often a dead zone where the stock enters a period of price hibernation.

However, if the management is sufficiently motivated and the geological setting permits, the company can push the project further along the curve via an aggressive exploration campaign, creating additional shareholder value with the drill bit.

I like these kinds of setups.

Our shortlisted Skeena Resources (SKE.V) fits into this category, as does Pure Gold (PGM.V).

Minnova Corp (MCI.V)

- 37.08 million shares outstanding

- $9.27M market cap based on its recent $0.25 close

In a nutshell, Minnova offers the potential for a robust (near term) production scenario, plus significant (high-grade) exploration upside.

Minnova’s flagship asset is its past-producing PL Gold Mine in the prolific Flin Flon – Snow Lake Greenstone Belt of Central Manitoba.

The project was in production for two years in the late 1980s. The previous operators, lacking the skillsets required to mine narrow high-grade veins, shuttered the operation, and it has remained on care and maintenance since.

Minnova acquired the project back in 2011, at the tail-end of the previous bull cycle in gold (the following is a monthly chart that takes us back one decade):

Since acquiring the property, Minnova has been methodically pushing it further along the development curve via multiple drill programs and economic studies.

Let’s motor through the fundamentals here.

The current global resource is > 700k ounces of high-grade material.

The resource has an underground and open-pit component at both the main LP deposit, and the satellite Nokomis deposit.

Regarding the mineralization making up these ounces-in-the-ground, there may be an issue with the accuracy—a positive issue. Due to the coarse nature of some of the mineralization encountered in drilling, it’s possible that the resource has been understated.

What really lies in LP’s subsurface layers could be more… a development that would have a positive processional effect on everything, particularly the economics of the project.

We’ll talk about this issue in future articles.

There’s a 1,000 tpd permitted mill on the property. The replacement cost of said mill is > $60M.

The project is fully permitted—the timeline to production is short should the company decide to raise the necessary funds and begin breaking ground.

This is a modest production scenario—roughly 45k ounces per annum. Management envisions reopening the underground mine as well as carving out several small open pits.

The above-noted mill will be fired back up with conventional crushing/grinding, a gravity circuit, flotation, regrinding, and cyanidation followed by the Merrill-Crowe recovery process—one of the most widely used methods for gold and silver recovery.

It’s a modest mine plan, but the economics are incredibly robust.

A Feasibility Study (FS) tabled back in 2017, using a US $1,250 gold price, demonstrates the following values:

- An after-tax NPV at a 5% discount rate of Cdn $36.7 million

- An after-tax IRR of 53%;

- A LOM OPEX = Cdn $162/tonne–US$750 /oz;

- Total estimated CAPEX = Cdn $35M;

- A swift payback period of ~1.5 years.

Those are some decent numbers in their own right. But a US $1,250 gold price input is far too conservative (consult the price chart at the top of the page).

If we factor in a more realistic US $1,875 gold input, we get:

- An after-tax NPV at a 5% discount rate of Cdn $185.62M

- An after-tax IRR of 184%

If we factor in US $2,000 gold (and let’s face it, we’re nearly there)…

- An after-tax NPV at a 5% discount rate of Cdn $215.38M

- An after-tax IRR of 209%

All of a sudden it’s not looking so modest.

These kinds of numbers/values leave all kinds of room for shit-happens. The leverage to buoyant Au prices is outstanding.

When the company tabled these higher inputs last week, they stated the following:

“Readers are cautioned that the above sensitivity analysis only considers a single change in a variable (i.e. the change in price of gold) and does not consider any changes in other variables that may have occurred since the completion of the 2017 FS.”

Fair enough.

Another intriguing element of this play is the exploration upside. The company hasn’t tested the potential—some 20-plus kilometers of geologically prospective ground—outside the main resource area… until very recently.

To set the stage for a drilling campaign, the company announced the closing of a modest non-brokered raise on July 16th:

Minnova Corp. Announces Closing of Non-Brokered Private Placement

This PP of flow-through units was priced at $0.20 for gross proceeds of $855,000. Each unit consisted of one FT share and one half of a 2-year $0.25 warrant. The warrants are subject to an acceleration clause where if the shares trade at $0.375 for 20 consecutive trading days, the company may accelerate the warrants giving the warrant holders 30 business days to pony up.

I suspect these acceleration clauses may become more and more an issue with warrant holders as share prices can rip higher, on any positive development, in a NY Minute these days. These warrants will stoke the treasury with another $534k, if (when) exercised.

I like that the company chose to raise a modest amount of funds this go-round. Management appears keen to keep the share structure tight. Speaking of which…

There is some debt on the books—roughly $1.7M—but it should be manageable, especially in this market.

Back to the exploration upside…

That’s the real kicker here—the potential along Minnova’s share of this prolific greenstone belt—20-plus kilometers outside the main resource areas—is virtually untouched.

Geologically speaking, the PL Deposit consists of multiple, stacked shear zones that trend northwest to southeast. This is a narrow, high-grade vein system.

The red lines streaking along the bottom right of the above map represent the veins structures included in the PL deposit mine plan. Note the drill targets along strike, to the northwest.

Select highlights from a 2017 infill drilling campaign include:

- 23.79 g/t over 1.00 meter;

- 23.28 g/t over 1.00 meter;

- 15.76 g/t over 1.00 meter;

- 298.05 g/t over 0.30 meters;

- 81.90 g/t over 0.78 meters;

- 70.35 g/t over 1.04 meters;

- 23.28 g/t over 0.65 meters;

- 32.25 g/t over 1.00 meter;

- 27.02 g/t over 1.00 meter;

- 21.69 g/t over 0.95 meters;

- 23.90 g/t over 1.17 meters;

- 12.70 g/t over 1.00 meter;

- 12.40 g/t over 1.00 meter.

A stepout drilling campaign during the winter of 2017/2018 tagged the following results:

- 13.5 g/t over 1.00 meter;

- 16.0 g/t over 1.00 meter;

- 6.15 g/t over 1.00 meter;

- 6.85 g/t over 2.00 meters.

More recently—just last week—the company dropped the following headline:

“The drill program calls for approximately 2,000 meters of drilling focused outside of the current PL mineral resource and reserve to demonstrate the exploration and resource expansion potential on the permitted mining lease. Following the conclusion of the drill program work will shift to property wide surface exploration and prospecting to trace the strike extensions of the PL deposit trend, the PL North Extension Trend and an emerging new trend identified in current drilling hosted within the footwall Tonalite.”

This is an interesting development for the company—an emerging new trend—one that could move the needle in a big way.

The following table is a summary (with geologist observations) of the mineralized intercepts encountered in this recently initiated drilling campaign.

The holes were designed to test the vein structures at shallow depths (50 meters to 150 meters).

All of these intercepts are located within 350 meters of the PL Gold Mine infrastructure.

“Results to date appear to be defining a new mineralized vein/structure within the Tonalite that typically occurs in the footwall of the main PL deposit. If the assay results confirm the visible gold observed in the core the area could be rapidly advanced with additional drilling and included in a future NI 43-101 resource estimate and possibly included in an updated feasibility study.”

Gorden Glenn, Minnova CEO:

“The PL Mine Mineral Lease and surrounding property have exceptional exploration and resource expansion potential. This drill program was designed to demonstrate the on-lease exploration potential. We are pleased to see a new mineralized vein/structure emerging in the Tonalite where visible gold has been observed in core on our initial 2 holes. We encourage our shareholders and new investors to watch our social media accounts for pictures and updates on our 2020 summer drilling and exploration program.”

There’s more to the Minnova story, but we’ll leave it for another day.

I’d be remiss in not crediting Vince Marciano for prompting me to elevate Minnova to shortlist status. I’ve been following the company’s progress over the years, but Vince nudged me a few days back, updating recent developments I had yet to consider, namely the geologist observations of the mineralized intercepts encountered during this ongoing drilling campaign.

One last note re Minnova before we move on…

Order execution is crucial with low liquidity plays like Minnova. I’d avoid using market orders and enter buy-orders carefully, cautiously (you could create your own personal bull market with a mere $10k market order).

Elsewhere in the Highballer shortlist portfolio

Forum was recently featured in my Equity Guru round-up piece—Equity.Guru’s sub-$20m ExploreCo shortlist: mining microcaps that are fit to follow (part 1 of 2)—and word appears to be getting out re this undervalued, district-scale copper play in a vastly under-explored region of mining-friendly Saskatchewan.

Things are busy at Forum Central, and it’s about to get much busier.

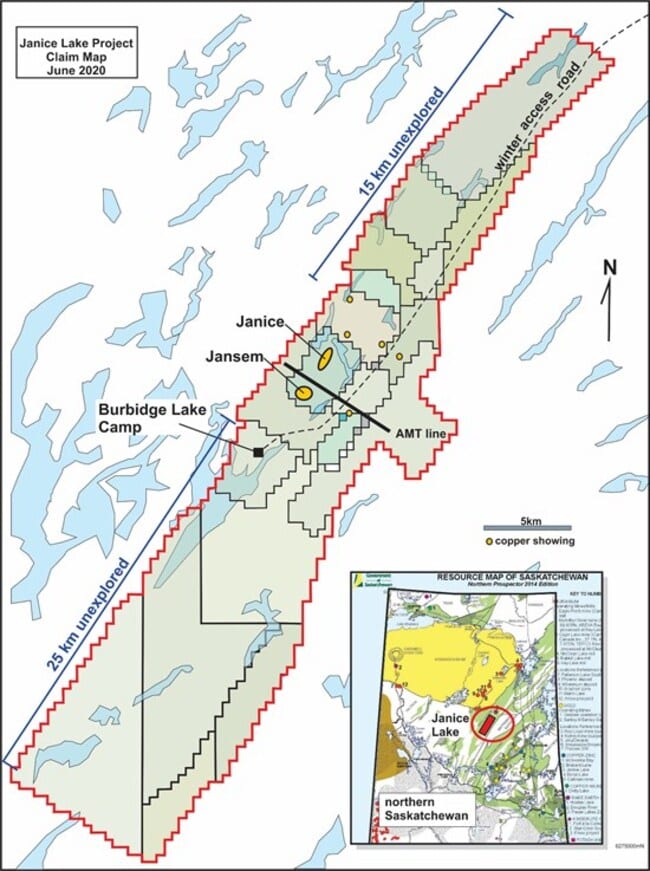

To review, Forums flagship asset is Janice Lake—38,250 hectares located in north-central Saskatchewan within the Wollaston Domain, “a northeasterly-trending belt of metamorphosed lower Proterozoic supracrustal rocks deposited upon Archean granitoid basement.”

Forum controls all 52 kilometers of the Wollaston Copper belt.

The property boasts over 20 sediment-hosted copper showings that hold the potential for multiple layers of copper mineralization.

A 1993 drilling campaign by Noranda tagged an interval of 0.77% Cu over 33.0 meters (including 1.6% Cu over 6 meters) within 35 meters of surface.

A modest drilling program by Phelps Dodge cut 0.72% Cu over 26.0 meters (including 1.33% Cu over 5.83 meters) in a separate zone.

More recently, a surface sampling campaign by Transition Metals (XTM.V) yielded grab sample values ranging from 0.34 to 9.35% copper, and 0.7 to 61.7 g/t silver.

A first pass, four-hole drilling campaign conducted by Forum in the summer of 2018 tagged a highlight interval of 18.5 meters grading 0.94% Cu and 6.7 g/t Ag (including 5.2 meters grading 2.22% Cu and 16.5 g/t Ag).

Building on the momentum from that 2018 campaign, Rick Mazur, Forum’s CEO, brought in Rio Tinto and tabled a JV deal worth $30M.

Copper is Rio’s #1 target commodity.

The work commitments hashed out in this JV agreement are substantial—it puts Forum in an enviable position.

Rio is a mining behemoth. They never get involved in a project unless it holds the potential for a world-class orebody. Rio’s interest and financial commitment to Janice Lake add heaps of geological credibility/validity to the project.

Rio’s first pass with the drill bit tagged the following values last summer:

- 0.41% Cu and 4.2 g/t Ag over 57.1 meters (from 78.9 meters to 136 meters), including 0.95% Cu and 9.7 g/t Ag over 13 meters (from 89 meters to 102 meters);

- 0.57% Cu and 1.50 g/t Ag over 51.8 meters (from 116.2 meters to 168 meters), including 1.09% Cu and 1.39 g/t Ag over 9.1 meters (from 118.9 meters to 128 meters) and 1.32% Cu and 3.42 g/t Ag over 5.0 meters (139.0 meters to 144.0 meters).

Rio obviously appreciated these early stage results.

The mining colossus spent $3.7 million at Janice Lake in 2019 and is accelerating work on the property projecting to spend $7 million on a multi-phase drilling campaign.

On June 23rd, the JV fine-tuned its Janice Lake objectives:

Rio Tinto Commences Exploration at Janice Lake Sedimentary Copper/Silver Project, Saskatchewan

The following excerpt from this late June press release lays things out neatly:

REGIONAL DRILLING – Copper showings, structural, geophysical, geochemical and boulder train targets developed by the mapping and prospecting program will be drilled using a Rotary Air Blast (RAB) drill rig. This will be a fast and cost-efficient method to test bedrock in areas of overburden for hidden copper/silver mineralization. Drilling permit applications for this work and a proposed future diamond drilling program are in process and are expected to be granted by mid-July.

Author’s note: This regional approach opens up the possibility of multiple new discoveries.

GEOLOGICAL MAPPING AND PROSPECTING – An eight person prospecting and mapping team has started systematic traverses on 2km wide spacings on the 52km extent of the property (see Figure 1). Detailed follow-up mapping and prospecting will be completed on prospective areas for strata-bound and structural copper/silver targets and mineralized areas discovered on the property by prospecting.

ORIENTATION SURVEYS – A program of geophysical and geochemical orientation surveys over the known mineralization at the Janice target that was drilled last summer has commenced. Exploration techniques such as Induced Polarization, electromagnetic, vegetation and soil surveys will be conducted over the deposit to identify signatures that may identify other deposits on the property. Downhole logging of the 2019 holes will be completed this summer and a regional AMT transect across the full 11.6 km width of the basin will be conducted to understand basin architecture.

CAMP CONSTRUCTION – Crews have begun construction of the 50 person camp on the property at Burbidge Lake. This camp will provide improved, proximal access for a proposed future diamond drilling program that would follow up on the Jansem and the Janice targets drilled in 2019, the Rafuse target 3 km to the north and new targets identified from this summer program.

CEO Mazur:

“I look forward to this summer’s program with a regional focus on uncovering the full extent of copper and silver mineralization at Janice Lake. We have barely scratched the surface on exploring this sedimentary basin which stretches for over 50 kilometres. Rio Tinto’s focus will not only be on finding higher grade and thicker open pit strata-bound horizons, but also high grade structurally controlled mineralization.”

News that JV partner Rio Tinto dropped a 43-101 on a large copper exploration project—a maiden Inferred resource at its 100% owned Winu copper-gold project in the Paterson Province of Western Australia—holds relevance where Janice Lake is concerned.

Rio is on the hunt for these monster sedimentary deposits and is targeting these Proterozoic Eon prospects. It was during this period of our planet’s evolution that a lot of copper was deposited throughout our subsurface layers.

I mentioned earlier that copper is Rio’s #1 target commodity. The reasons, as per the products page on Rio’s website…

Copper increases energy efficiency

- Copper is the best non-precious-metal conductor of heat and electricity on the planet, so items that contain copper tend to operate more efficiently. According to the International Copper Association (ICA), using more copper in motors and appliances can reduce carbon dioxide emissions by 1.25 gigatonnes – equivalent to taking half a billion cars off the road.

Copper helps renewable energy systems work better

- Renewable energy systems – like solar, wind and hydropower – rely on copper to generate and transmit energy with maximum efficiency.

Copper is critical to greener vehicle technology

- Copper is the primary conductor in the world’s electrical infrastructure, contributing to the electrification of transportation. For example, electric vehicles have a copper intensity 3-4 times higher than traditional vehicles.

The chart for the metal itself is also looking constructive, pushing dramatically higher since the crash event of March 16, 2020, and then consolidating in its current narrow trading range…

Leaping over property boundaries, on July 27th, the company dropped the following headline re its Love Lake project:

The 27,896 hectare Love Lake Ni-Cu-PGM project is located 60 kilometers northeast of Janice Lake.

Love Lake is early stage, but the company isn’t hesitating in pushing it further along the curve.

Quoting directly from this July 27th press release:

“Forum has contracted SHA Geophysics Heli-GT system that measures the earths’ magnetic gradient in two horizontal directions as well as in a vertical direction, providing an accurate measurement of the magnetics with only minimal noise. Approximately 3,500 line kilometres will be surveyed on a 100m line spacing, covering the majority of the Love Lake project, and the survey should take approximately 10 days to complete. Drill targets defined by the airborne survey will be followed up by ground mapping/sampling this summer and electromagnetic surveys this fall/winter.”

Characterizing the project, the press release went on to state:

“The property is prospective for Nickel-Copper massive sulphide deposits in feeder zones (Voisey’s Bay, Chalice Gold), Lac de Iles-type structural platinum/palladium deposits and reef-type platinum/palladium deposits. The Ni-Cu-PGM occurrences are associated with the Love Lake gabbroic pluton within the 2.5 billion year old Swan River mafic complex in the Peter Lake Domain. Forum staked a 20 km by 12 km area of historic copper- nickel platinum group metal showings. Grab samples in Trench #4 in the What Lake area returned 0.33% Cu, 1.33% Ni, 2.73 g/t platinum, 2.68 g/t palladium, 70 ppb gold plus 0.43%Cu, 0.23% Ni, 3.58 g/t platinum, 4.27 g/t palladium, 200 ppb gold.”

“An area 3km to the southwest of the What Lake occurrence discovered copper mineralization by trenching over a 1.4 kilometre strike length. Two holes drilled in 1968, 68-10 and 11, returned 31.7m of 0.23% copper and 36.6m of 0.29% copper respectively and have never been followed up.”

With the commencement of drilling at Janice Lake only days away, Forum is on the cusp of generating a substantial volume of drilling-related newsflow over the balance of 2020, and well into 2021.

Very briefly (to prevent this one from turning into War and Peace)…

Strategic Metals (SMD.V) announced the commencement of drilling at their wholly owned Mount Hinton project in the Keno Hill region of the Yukon via the following July 27th headline:

The key takeaway here:

“The program is fully funded with adequate contingency to double the amount of drilling, if results and weather permit.”

Pure Gold (PGM.V) recently announced underground exploration drill results—step-out holes drilled in close proximity to existing underground development.

Underground Drilling at PureGold Red Lake Mine Intersects 12.8 g/t Gold Over 10.0 Metres

“Drilling has extended gold mineralization out from current design stopes, has discovered new gold zones that will be integrated into mine planning, and has confirmed stopes scheduled for near term production.”

Highlights from this batch include:

- 12.8 g/t gold over 10.0 metres from drill hole PGU-0136; including

20.1 g/t gold over 5.0 metres; - 9.3 g/t gold over 2.4 metres from drill hole PGU-0123; including

16.2 g/t gold over 1.1 metres; - 10.6 g/t gold over 2.0 metres from drill hole PGU-0124.

Darin Labrenz, PureGold CEO:

“These latest high-grade gold intercepts continue to reinforce our near-term growth plan for the PureGold Red Lake Mine and to exhibit the tremendous strength, continuity and scalability of this high-grade gold system. Underground exploration drilling continues to extend stopes that are part of our near term mine plan, and to discover brand new gold zones which could have a direct net positive impact on our production profile, and because of their proximity to existing development a potential impact to near term cash flow at our mine. In this case we have more than doubled the strike length of a planned stope, further demonstrating the dramatic transformative growth potential of our PureGold Mine. We have only just begun a 30,000 metre exploration program, which will span across our seven kilometre gold corridor, and already we’re delivering on our objective of building a multigenerational mining complex in Red Lake, Canada.”

END

Greg Nolan

Full disclosure: Minnova is not a Highballer marketing client. The author does not own shares. Though I have an interest in getting positioned in this stock, I’ll wait at least three trading days before initiating any such purchases.

Forum Energy Metals is a Highballer marketing client. I own shares in the company. Consider me biased.

Strategic Metals is not a Highballer marketing client. I own shares in the company. Consider me biased here too.

Disclaimer - Legal NoticeHighballerstocks.com (Greg Nolan) is not a licensed financial advisor and does not give investment advice.

The content of this report is for information purposes only.

Nothing contained herein should be construed as a recommendation or solicitation to buy or sell any security.

Always consult a licensed qualified investment advisor in your legal jurisdiction before making any investment decisions.

Though Highballerstocks.com (Greg Nolan) believes its sources to be credible, and the statements contained herein to be true, readers must conduct their own thorough due diligence, and or consult with a qualified investment advisor before important investment decisions are made.

Highballerstocks.com (Greg Nolan) accepts no responsibility or liability for the accuracy of the contents of this report.