In an earlier offering, we talked about peak gold, lean project pipelines and how that is forcing producing companies to hunt:

Fact: every day a Gold Producer digs ore out of the ground—every day they’re in business—their precious metal inventory shrinks.

Whether it’s a Senior, a Mid-tier, or a Small Producer, the key to long-term survival is a robust pipeline of new discoveries.

If a company is unable to grow this project pipeline organically, through exploration, it needs to change tactics. It needs to take on the role of acquirer, predator.

The true speculators among us will view the task of shortlisting potential takeover candidates as a game. But a game where, if right, an enormously profitable endgame will come into play (endgame is a concept we’ve explored in these pages too).

So where might a resource-hungry producer look to acquire a vulnerable junior with desireable ounces-in-the-ground? The first place I would look is right next door, down the road. Acquiring an economic orebody within trucking distance of one’s existing operation is a no-brainer—the synergies are many. More on this little brainstorm further down the page.

A new add to our list

Last week we took a close look at what I believe to be one of the better plays in the Yukon—White Gold Corp (WGO.V).

We’re still in the Yukon, taking a look at a company further down the food chain, but with solid exploration potential in close proximity to two larger entities that may be on the hunt.

The company is Banyon Gold (BYN.V).

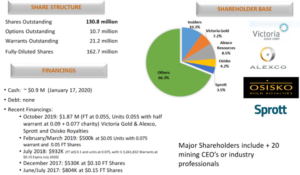

- 130.82 million shares outstanding

- $7.85M market cap based on its recent $0.06 close

Banyan is exploring two projects in the Yukon—the Hyland Gold Project and the Aurex-McQuesten Property.

The 18,620 hectare Hyland project is located in the Watson Lake Mining District of the southeast Yukon.

Hyland’s ‘Main Zone’ backstops Bayan’s modest valuation ($7.85M based on recent trading patterns) with an Indicated resource of 236,000 AuEq ounces at a grade of 0.85 g/t, plus an Inferred resource of 288,000 AuEq ounces at a similar grade.

The Main Zone is open in all directions and at depth. We should see a modest drilling campaign on the property in the coming months.

Main Zone drilling highlights:

- 85.0 meters of 0.73 g/t Au and 5.61 g/t Ag;

- 36.24 meters of 1.3g/t Au and 2.54 g/t Ag;

- 57.4 meters of 0.90 g/t Au and 3.3 g/t Ag;

- 94.6 meters of 0.70 g/t Au and 7.0 g/t Ag;

- 46.0 meters of 1.6 g/t Au and 6.5 g/t Ag.

With a >18 kilometer long structural corridor, multiple untested drill targets open up the potential to grow this resource significantly.

The company is seeking a joint venture partner to push Hyland further along the development curve.

2019 newflow was all about the company’s Aurex-McQuesten project.

Aurex-McQuesten:

- 92.30 square kilometer land package with regional resource potential;

- Prospective ground between a producing mine and an advanced stage development project;

- Multiple known near-surface undrilled gold targets;

- An Intrusion related gold system;

- Road access, a three-phase power line, key infrastructure (the project even has cell phone reception);

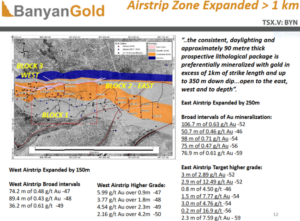

The McQuesten Gold Zone and Airstrip Zone are characterized by a 5.2 square kilometer Au/Ca soil anomaly and long intervals of shallow, low-grade material.

Near-surface Airstrip Zone drilling highlights:

- 0.74 g/t Au over 113.0 meters;

- 0.64 g/t Au over 94.9 meters;

- 1.06 g/t Au over 80.8 meters;

- 0.74 g/t Au over 96.4 meters;

- 0.66 g/t Au over 107.7 meters;

- 0.94 g/t Au over 71 meters.

Higher-grade intervals include:

- 5.0 g/t Au over 5.3 meters from 94.7 meters;

- 3.2 g/t Au over 11.8 meters from 89.3 meters;

- 3.1 g/t Au over 8.84 meters from 127.4 meters;

- 112.3 g/t Au over 0.1 meters from 18.2 meters.

In mid-Nov, 2019, the company announced an expansion of the zone to >1 kilometer.

Banyan is advancing this zone rapidly.

Yep, some of these Airstrip Zone hits are low grade, but the intervals are long, close to surface, potentially open-pittable, and surrounded by key infrastructure (future economic studies could present some very agreeable Opex and CapEx numbers).

The new higher-grade Powerline Zone—a parallel structure—located 1 kilometer to the south of Airstrip, is where the company believes it can add significant ounces.

Powerline begins at surface and is open in all directions from the 250-meter x 250-meter area drilled to date.

According to the company’s geological model, it’s possible that Powerline and Airstrip’s subsurface mineralization will hook up, forming one long zone. That would bring the predators in for a closer look.

Power Zone highlights:

- 2.89 g/t Au over 4.6 meters;

- 1.46 g/t Au over 7.4 meters;

- 1.42 g/t Au over 4.6 meters;

- 48.1 g/t Au over 0.4 meters;

- 1.24 g/t Au over 4.2 meters;

- 4.57 g/t Au over 1.5 meters;

- 2.05 g/t Au over 4.3 meters;

- 5.68 g/t Au over 1.5 meters;

- 0.49 g/t Au over 97.9 meters (including 1.34 g/t over 24.5 meters);

- 0.35 g/t Au over 78.5 meters;

- 0.47 g/t Au over 45.5 meters;

- 0.78 g/t Au over 13.4 meters.

A maiden resource for the Aurex-McQuesten Gold Project is expected in Q2 of this year.

Back to predator and prey

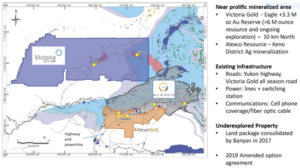

There are two larger entities in close proximity to Banyan—Victoria Gold and Alexco Resources.

Victoria’s Eagle Gold Project has evolved from a development project to an operating mine.

Construction at Eagle Gold was completed in early July of 2019, one month ahead of schedule, and the ramp up phase began in September.

Gold Eagle’s technical fundamentals:

- Reserves of 3.3 million ozs Au;

- Annual production of roughly 220,000 ozs Au;

- Cash Cost per Au ounce of US$577;

- All-in Sustaining Cost per Au ounce of US$774;

- Post-tax NPV @ 5% discount = $1,034 million.

The last 13 years for Alexco has seen a systematic approach to exploration and development.

A 2019 Prefeasibility Study (PFS) demonstrates high-grades, robust economics, and an extremely modest CapEx:

- An after-tax net present value NPV (5%) of $101.2 M;

- An after-tax internal rate of return of IRR of 74%;

- All-in sustaining costs (AISC) between $11 to $12.00;

- Capital expenditures (CapEx) a very modest $23M.

Current mineral reserves and resources according to this 2019 PFS mine plan (incorporating the company’s Birmingham and Flame & Moth deposits) stand at:

- +74 million ounces of silver in the Indicated category (3.88 Mt @ 594 g/t Ag) – including 30.5 million ounces in the Probable Reserves category (1.18 Mt @ 805 g/t Ag);

- +24 million ounces of silver in the Inferred category (1.66 Mt @ 455 g/t Ag).

Clearly, these are solid mining scenarios.

Both of these companies may be looking to increase their exposure to the region.

Bayan’s ounces-in-the-ground, should they begin to pile up over the course of the next field season or two, would be a no-brainer acquisition target either of these two.

Actually, both companies have already made a move into Banyan common—note the positions currently held (management has skin in the game too).

It doesn’t take a rocket scientist to see the endgame here.

Of course, the truth machine will have the final say.

Final thoughts

I’m wary of these early-stage projects, but Banyan is backstopped by a resource and a large geological footprint. There is good resource expansion and discovery potential here.

What I find especially compelling about this company is its management team—a crew with broad experience in exploration, development, and permitting projects in the Yukon.

The 92 square kilometer Aurex-McQuesten property has seen little modern exploration. The maiden resource (expected Q2) and 2020 drilling will give us a much better picture of what may ultimately lie in these subsurface layers.

As of Jan. 17, the company had $900k on its books—that’s enough to launch a fairly substantial drilling campaign at Aurex-McQuesten where costs run a modest $200 per meter.

We stand to watch.

END

—Greg Nolan

Full disclosure: the author does not currently own shares in Banyan though he may initiate purchases in the coming weeks.

Disclaimer - Legal NoticeHighballerstocks.com (Greg Nolan) is not a licensed financial advisor and does not give investment advice.

The content of this report is for information purposes only.

Nothing contained herein should be construed as a recommendation or solicitation to buy or sell any security.

Always consult a licensed qualified investment advisor in your legal jurisdiction before making any investment decisions.

Though Highballerstocks.com (Greg Nolan) believes its sources to be credible, and the statements contained herein to be true, readers must conduct their own thorough due diligence, and or consult with a qualified investment advisor before important investment decisions are made.

Highballerstocks.com (Greg Nolan) accepts no responsibility or liability for the accuracy of the contents of this report.