This is a good time to update a few of the companies I follow closely here at Highballerstocks. Most have recovered significant ground off their March 16 crash lows, some more than others.

Apparently, the COVID-19 threat exists even in the remote, wide-open expanses where junior exploration companies are drilling high priority targets. A number of companies that have scaled back operations, some by gov’t mandate, until the dust settles.

I spoke with several ExplorerCo execs over the past week. Clearly, there is a sense that the tide is turning; that the opportunity is ripe, and now is the time to begin creating shareholder value with the drill bit.

In the meantime, geological models will be updated, drill targets will be prioritized, resource updates and economic studies will be pushed towards fulfillment.

When the activity curbs are lifted, these companies will be ready to hit the ground running.

Cartier Resources – (ECR.V) – (ECRFF.OTC)

- 191.63 million shares outstanding;

- $17.25M market cap based on its recent sub-dime close;

- roughly $6.2M in cash.

Two-month price chart:

There are two companies on our shortlist that are currently getting little in the way of love from the market. Cartier is one of them, despite recent positive developments and a treasury stoked to the tune of $6.2M.

Brief summary:

Cartier is developing its Chimo Mine Project where a phase 3 drilling campaign is opening up the project’s resource potential at depth.

The company also boasts a robust project pipeline. We’ll hear more about these projects in due course.

Early last November, the company released a maiden resource for its Central Gold Corridor:

- 3,263,300 tonnes at an average grade of 4.40 g/t Au for a total of 461,280 ounces of gold in the Indicated category;

- 3,681,600 tonnes at an average grade of 3.53 g/t Au for a total of 417,250 ounces of gold in the Inferred category.

A common theme affecting many companies operating in Canada applies here too: all drilling activities are temporarily suspended at Chimo until virus infections flatline.

The March 26 news stated that work continues on the Chimo project as follows:

- The resources estimate in progress at the North Gold Corridor and South Gold Corridor continues (image);

- Mapping and sampling of core from the current drill program along the geometric extensions below the new Zones 5B4-5M4-5NE continues (image);

- Internal engineering studies aimed at optimizing resources and ongoing exploration drilling continues.

Additionally, CEO Philippe Cloutier will be doing a live broadcast on Twitter tomorrow, April 1st…

Cartier deserves better than it’s getting from the market. As the uptrend in gold continues to assert itself over the coming weeks and months, these shares should respond accordingly. And like the vast majority of the companies featured in these pages, Cartier has endgame potential.

Coral Gold (CLH.V) – (CLHRF.OTC)

- 46.14 million shares outstanding;

- $19.61M market cap based on its recent $0.425 closing price;

- $14M in cash.

Two-month price chart:

Brief summary:

Coral holds an uncapped sliding scale 1% to 2.25% NSR on over 2.7 million ounces at Barrick Gold’s Robertson Property located along the prolific Cortez Gold Trend of northern Nevada.

Robertson is a joint venture between Barrick (61.5%) and Newmont-Goldcorp (38.5%). This JV among mining behemoths is called Nevada Gold Mines—NGM for short.

The following map shows Pipeline, Cortez Hills and Goldrush (three of the largest Carlin-type gold deposits on the planet) and their on-trend proximity to Robertson.

Pipeline, Cortez Hills and Goldrush make up NGM’s lowest-cost assets with over 50 million reserve & resource ounces.

Coral is in a sweet spot with this NSR. This royalty goes beyond the 2.7 million ounces defined in the current resource—it covers the depth potential of these subsurface layers. The geological setting at Robertson is ripe for another Meikle-style deposit at depth (from 2007 to 2016, the Meikle underground mine produced over 4 million ounces of Au at an average grade of .295 oz/ton).

The company also maintains several early-stage exploration projects in the Crescent Valley region along Cortez Gold Trend.

As mentioned in a previous offering, Coral’s share price was nearly cut in half during the March 16 liquidity event. It has since stabilized in a familiar $0.45 trading range.

Earlier this month, the company provided an update on NGM’s progress at Robertson:

- NGM recently delivered its summary of work completed in Q4 2019 at Robertson, reporting that 1,675 meters of geotechnical drilling has been completed.

- NGM are progressing with updating the geological model, preparing mine plans, confirming metallurgical assumptions and carrying out baseline study work.

- Barrick recently mentioned a mineral resource at the Robertson Project in their 2019 fourth quarter report, and while the details of the new resource estimate have not yet been made public, they indicate the Robertson property is now considered part of the mineral resource base for the Cortez Mine complex. Coral Gold Management is encouraged by the progress on the Robertson Project, especially that a new mine design was created, and work progresses towards development of this property.

Progress is being made at Robertson—the company maintains a strong cash position and a super-tight cap structure while the deposit gets pushed further along the development curve.

HighGold Mining (HIGH.V) – (HGGOF.OTC)

- 33.34 million shares outstanding;

- $26.68M market cap based on its recent $0.80 close;

- $12M in cash.

Two-month price chart:

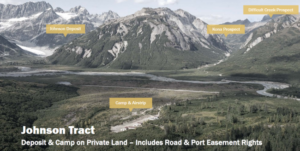

As noted in my maiden HighGold article, and not to diminish the geological prospectivity of their Timmins assets, the company’s Johnson Tract property in southcentral Alaska is where the real excitement lies.

An excerpt from said article:

Johnson Tract was discovered by Anaconda back in 1982.

Anaconda’s discovery hole tagged an incredible 108.6 meters grading 10.39 g/t gold, 7.64% zinc, 0.71% copper, 2.01% lead and 8.1 g/t silver (including 48 meters grading 21.1 g/t gold, 9.93% zinc, 0.88% copper, 2.86% lead and 12.3 g/t silver).

Those are some crazy high-grade values. And it’s not often you find high-grade gold AND base metals together in the same deposit.

Equally compelling is the fact that this project has been hidden from the market for decades. No exploration—zip, zero, nada—has been conducted on the property in over 25 years.

Between 1982 and 1995, 88 holes were drilled on the project for a total of 26,840 meters. These historic drilling campaigns tagged multiple 50 to 100-meter intercepts grading 10 g/t Au or better.

Grades and widths this fat are not easy to come by nowadays. It’s the main reason we’re here.

As reported in a recent offering, HighGold suspended its drilling activities in the Timmins camp after drilling 12 drill holes for 2,524 meters of a planned 5,000-meter program.

Worth watching, CEO Darwin Green delivered the following presentation at the Metals Investor Forum one month back. Green does a good job of summarizing the tremendous latent potential of the Johnson Tract project. The following link will take you there.

Darwin Green, CEO of Highgold Mining at Metals Investor Forum on Feb 28-Mar 1, 2020 in Toronto

This is a top-shelf ExplorerCo with a tight market cap.

Skeena Resources (SKE.V) – (SKREF.OTC)

- 124.45 million shares outstanding;

- $99.56M market cap based on its recent $0.80 close;

- > $40M in cash.

Two-month price chart:

Brief summary:

Skeena’s Eskay Creek Project ranks as one of the highest grade open pit deposits on the planet, boasting a resource of some four million ounces grading 4.4 g/t AuEq.

A recently tabled PEA demonstrates an after-tax IRR of 51% using a US$1,325 gold price.

For a deeper delve into the company, there’s this:

This is another top-shelf company.

The biggest news out of the Skeena camp in recent sessions was a sizable $20M PP (17,316,000 flow-through shares) priced at $1.155 per share.

Today (Mar. 31), the company closed the first tranche ($15M) of the offering.

It also upsized the PP by 50%, to a cool $30M. There’s an appetite for this stock, and for good reason.

“Due to strong demand for flow-through shares from outside of British Columbia, the Company has upsized the offering to C$30 million and has added a National flow-through component at $1.05 per share. The Company expects to close the balance of the Offering in mid-April.”

There has been no mention of any curtailment of activities at Eskay Creek.

White Gold (WGO.V) – (WHGOF.OTC)

- 124.79 million shares outstanding;

- $64.89M market cap based on its recent $0.52 close;

- $5M in cash (give or take).

Two-month price chart:

White Gold is the other ExplorerCo on our shortlist that deserves love but isn’t getting any from Mr. Market.

Quick summary:

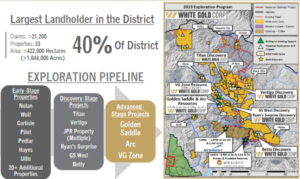

The company’s Golden Saddle and Arc deposits hold over 1.5 million resource ounces.

- 1,039,600 gold ounces within 14,330,000 tonnes at 2.26 g/t Au in the Indicated category;

- 508,700 gold ounces within 10,696,000 tonnes at 1.48 g/t Au in the Inferred category.

The VG Zone, located across the river from these two deposits, holds some 230,000 ounces in the Inferred category.

A resource update for the Golden Saddle and Arc deposits is on deck and could drop at any time.

White Gold hasn’t produced news in recent weeks, but its share performance is worth commenting on.

White Gold is an anomaly. It would appear to have it all: highly competent management, a district scale portfolio of Yukon properties with considerable resource and discovery upside, a fairly tight share structure, and the potential for strong newsflow as the 2020 field season draws near.

The Yukon appears to be faring rather well with only five confirmed COVID-19 cases. That could bode well for the upcoming field season.

The company’s shares have recovered from their March 16 crash low of $0.41, but deserve better than the lowly range they’re currently stuck in.

I suspect we won’t have long to wait before news drops on the ounce-count front (Gldn Saddle and Arc).

If the company wants to keep pace with the momentum set in seasons past, they’ll need to raise funds at some point.

That’s it for now. I’ll be presenting a new pick for our shortlist portfolio this weekend. Till then, take good care.

END

Greg Nolan

Disclaimer - Legal NoticeHighballerstocks.com (Greg Nolan) is not a licensed financial advisor and does not give investment advice.

The content of this report is for information purposes only.

Nothing contained herein should be construed as a recommendation or solicitation to buy or sell any security.

Always consult a licensed qualified investment advisor in your legal jurisdiction before making any investment decisions.

Though Highballerstocks.com (Greg Nolan) believes its sources to be credible, and the statements contained herein to be true, readers must conduct their own thorough due diligence, and or consult with a qualified investment advisor before important investment decisions are made.

Highballerstocks.com (Greg Nolan) accepts no responsibility or liability for the accuracy of the contents of this report.