Last week I profiled what I considered one of the better values in the junior exploration arena…

Strategic Metals (SMD.V) tees up Mount Hinton for high-grade gold and silver

With a number of high quality gold and silver plays beginning to catch a bid in recent sessions, Strategic was an anomaly. An extensive project portfolio, a top shelf crew, an exciting high-grade flagship asset, and a healthy treasury—these shares should’ve risen in lockstep with the rest of the best. The market is only beginning to catch on now…

… but the stock is still waaaay undervalued.

Of the companies profiled earlier this year in the Highballer portfolio, several remain stalled out near their lows, a predicament that is unlikely to persist much longer.

Cartier Resources (ECR.V) is our Quebec based ExplorerCo boasting a significant development asset and a robust project pipeline.

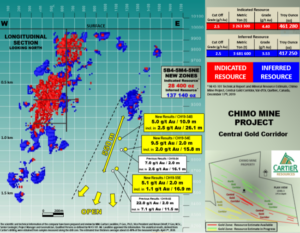

The company’s wholly owned Chimo Mine Project, a past producer of some 379K ounces of gold, continues to deliver resource enhancing results with the drill bit.

April 7 news: Cartier Intersects 5.0 g/t Au over 10.9 m, 250 m Below New Zones 5B4-5M4-5NE

Resources at Chimo currently stand at:

- 3,263,300 tonnes at an average grade of 4.40 g/t Au for a total of 461,280 ounces of Au in the Indicated category;

- 3,681,600 tonnes at an average grade of 3.53 g/t Au for a total of 417,250 ounces of Au in the Inferred category.

The Apr. 7 news release highlights mineralization below zones 5B4-5M4-5NE—zones that currently hold 165,540 resource ounces:

- 5.0 g/t Au over 10.9 meters (included within 26.1 meters grading 2.5 g/t Au), 250 meters below zones 5B4-5M4-5NE.

- 9.5 g/t Au over 2.0 meters (included within 15.8 meters grading 2.0 g/t Au), 350 meters below the zones 5B4-5M4-5NE.

The Apr. 7 release also highlights the discovery of a 4th gold zone within the East Sector—Zone 5CE—which returned 11.9 g/t Au over 2.0 meters.

The following map is marvelous in its detail. These new values are highlighted in yellow. Assay results released on Feb. 18, including 22 g/t over two meters, are highlighted in white:

Note the yellow arrows at the bottom of this map. Deposits in this region are known for their mineralized extensions at depth.

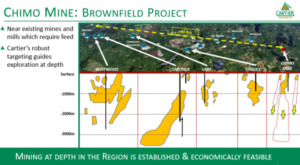

This next map is important—it demonstrates Chimo’s depth potential when compared to its neighbors…

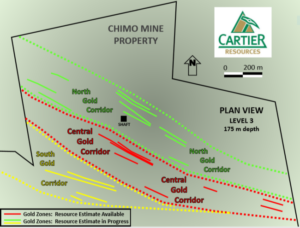

Near term catalysts include a resource estimate for the North and South Gold Corridor’s (map below), plus additional drill results from a multiple rig, 10,000-meter campaign designed to test for extensions at depth.

The company states that drilling is temporarily suspended due to C-19 restrictions but will resume as soon as said restrictions are lifted.

Chimo is an evolving story. The ultimate resource potential could approach 1.5 to 2 million ounces after the drill bit has its final say.

I’m betting this one has an endgame—a resource hungry predator taking Chimo out at a handsome premium. If (when) that happens, Benoist is on deck—the next project in line for a proper probe with the drill bit.

Though the stock bounced nicely off its March 16 crash-day lows, it’s still stuck in a sub-twenty cent trading range. That could change in a NY Minute once smart money types discover the latent value here.

Defense Metals (DEFN.V) is another stock in the portfolio that isn’t getting the respect it deserves.

The company’s wholly-owned 1,708-hectare Wicheeda Rare Earth Element (REE) Project in the Prince George region of mining-friendly B.C. boasts a number of fundamental features that set it apart from most development plays in this arena.

Two fundamentals factors that clearly standout:

1) The resource at Wicheeda currently stands at 11,370,000 tonnes averaging 1.96% LREEs (Light Rare Earth Elements).

A resource update is due.

Based on outstanding results from a 2019 drilling campaign, including two stepout holes grading 4.43% LREOs over 83 meters (inc 5.47% LREO over 33 meters) and 3.63% LREO over 75 meters (inc 4.01% LREO over 58 meters), we could see a significant revision in both tonnage and grade.

The current Wicheeda resource could be compared to a gold deposit grading 5.0 g/t (a grade of 1% LREEs is equal to roughly 2.5 g/t gold). With this in mind, examine all of the values encountered from recent drilling on the following map.

2) Wicheeda, with its positive metallurgy and mining friendly jurisdiction, is a politically strategic REE deposit. In response to supply concerns over China’s overwhelming domination of the REE market, Canada and the U.S. are moving to secure supply chains in their own back yards.

This is a matter of (tech) survival for the two nations. Earlier this year, the gov’t of Canada dropped the following headline:

Canada and U.S. Finalize Joint Action Plan on Critical Minerals Collaboration

“The Action Plan will guide cooperation in areas such as industry engagement; efforts to secure critical minerals supply chains for strategic industries and defence; improving information sharing on mineral resources and potential; and cooperation in multilateral fora and with other countries. This Action Plan will promote joint initiatives, including research and development cooperation, supply chain modelling and increased support for industry.”

The market has yet to recognize the significance of what Defense controls in its subsurface layers. Recent metallurgical test work has elevated Wicheeda to among the very best REE deposits on the planet.

Defense management is focused, pushing Wicheeda aggressively along the development curve:

Defense CEO Craig Taylor:

“With the decision to move forward with the flotation pilot plant, Defense Metals has achieved another key milestone towards advancement of the Wicheeda REE Project. Since announcing the option agreement to acquire the Wicheeda REE Project 14 months ago we have collected a 30 tonne bulk sample; produced a maiden mineral resource estimate; completed a highly successful 13 hole, 2,005 metre diamond drill program; and successfully developed a combined flotation and hydrometallurgical processing flowsheet for Wicheeda REE mineralization. This has allowed Defense Metals to exceed its Year 1 and Year 2 exploration spend commitments within the first 12 months.”

We shouldn’t have long to wait before the news begins to flow here. With a market cap of < $5M, this may be one of the more undervalued plays in the junior arena.

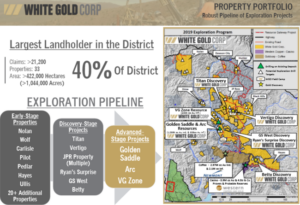

White Gold (WGO.V) appears to have it all: ounces-in-the-ground, multiple new (high-grade) discoveries, top-shelf management, unparalleled district scale exploration upside. So why the lack luster performance?

If you’re new to this story, the company holds a dominant land position in the White Gold District of Canada’s Yukon.

The Golden Saddle and Arc deposits hold the bulk of WGO’s resources.

- 1,039,600 gold ounces within 14,330,000 tonnes at 2.26 g/t Au in the Indicated category;

- 508,700 gold ounces within 10,696,000 tonnes at 1.48 g/t Au in the Inferred category.

Located directly across the river from the above resource, the VG Zone holds an Inferred resource of 230,000 gold ounces within 4.4 million tonnes at 1.65 g/t Au.

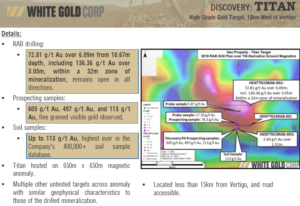

Of the multiple discoveries made in recent months, Titan and Vertigo stand out.

Note Titan’s uber high-grade values (above map).

With so many moving parts to this story, painting an accurate picture is difficult in such a limited space. My maiden White Gold article from two months back offers far greater detail (note the critical role soil samples play in this unglaciated part of the world)…

White Gold – unparalleled discovery potential in Canada’s Yukon

The company has been unusually quiet of late. But we shouldn’t have long to wait before an updated resource drops for Golden Saddle and Arc. We should also see a detailed plan for the upcoming 2020 field season.

As noted further up the page, the share price performance in recent weeks is puzzling, but this may represent an opportunity to accumulate shares in one of the very best exploration plays in the sector, at severely depressed prices.

Closing thoughts

In my estimation, every stock on my list—Skeena (SKE.V), HighGold (HIGH.V), Strategic (SMD.V), Pure Gold (PGM.V), Coral (CLH.V), and Banyan (BYN.V)—represents outstanding value at current levels. But the above three have yet to make a move off their lows. The time may be nigh for a push to higher ground.

END

—Greg Nolan

Disclaimer - Legal NoticeHighballerstocks.com (Greg Nolan) is not a licensed financial advisor and does not give investment advice.

The content of this report is for information purposes only.

Nothing contained herein should be construed as a recommendation or solicitation to buy or sell any security.

Always consult a licensed qualified investment advisor in your legal jurisdiction before making any investment decisions.

Though Highballerstocks.com (Greg Nolan) believes its sources to be credible, and the statements contained herein to be true, readers must conduct their own thorough due diligence, and or consult with a qualified investment advisor before important investment decisions are made.

Highballerstocks.com (Greg Nolan) accepts no responsibility or liability for the accuracy of the contents of this report.