Before we examine some very decent (infill) drill hole assays out of British Columbia’s Golden Triangle, here’s an excerpt from a piece I put up on Equity Guru earlier today…

The Fed can’t print gold (it can’t print silver either) – Pure Gold (PGM.V)

There’s rarely been a dull day in the gold (and silver) arena since the calendar turned over to 2020. The madcap volatility we’ve witnessed over the past few months has likely challenged the convictions of even the most hardcore of gold bugs.

There’s no shortage of opinions regarding where we go from here. For example, the Bank of America thinks gold’s technical momentum could push prices to an all-time high this year, even suggesting $3,000 is in the cards within the next 18 months.

$3,000.00 gold? You need to ask yourself, “Do I really wanna live in a $3k gold world”? The current financial landscape is bleak enough as is. I hate to imagine the view outside my window in a $3k gold world. But then again, I can can offer at least a dozen reasons why $3k should already be in our rear view mirror. Gold ended the NYMEX session on Friday (April 24) at $1,745 and change, btw.

The logic underpinning such a move—a doubling in price—is reasonable enough: as economic activity contracts, as fiscal spending ramps up, and as central banks around the globe expand their balance sheets at rates that defy description (I need better adjectives to more accurately chronicle this madness), gold will be viewed as the safest of safe havens.

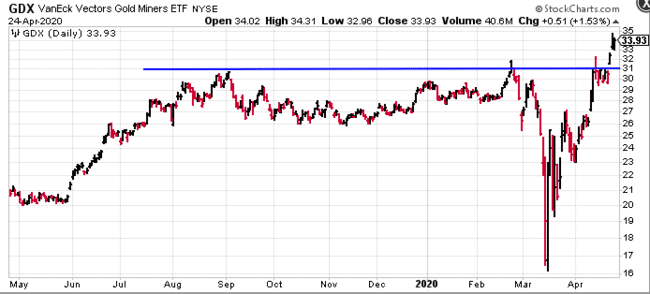

It’s interesting to note that the GDX (a proxy for our largest gold Producers) is currently challenging a resistance zone that has held the sector in check for going on seven years (blue line, chart below).

Zooming in closer with a one year chart, the drama and volatility in recent trading leaps off the page…

This is the kind of price action we want to see in these larger entities.

Skeena Resources (SKE.V) – (SKREF.OTC)

Further down the food chain, in the junior exploration arena, high-quality companies like Skeena could also be on the cusp of significant upside price trajectory.

Skeena management continues to push its flagship Eskay Creek Project further along the development curve having recently launched a 28,000 meter, multiple rig drilling campaign.

Eskay Creek went into production in 1994 after an intense bidding war wrestled the deposit away from its original (junior) owners—Consolidated Stikine and Calpine Resources.

During its peak, Eskay Creek was THE highest-grade gold producer on the planet. It produced some 3.3 million ounces of gold at a grade of 45 g/t and 160 million ounces of silver at a grade of 2,224 g/t. That’s a gold equivalent grade of > 2.5 ounces per tonne.

The mine produced for the better part of 14 years, finally winding down operations in 2008.

Due to the remoteness of the project and a low gold price environment, the cutoff grades applied to the deposit were exceptionally high—up to 30 g/t Au.

With markedly higher precious metals prices and significant improvements to the region’s infrastructure, sub-economic ore leftover from the historic operation appears to offer compelling economics today (note the project’s PEA further down the page).

Skeena now boasts one of the highest grade open pit development projects in the world—some four million ounces grading 4.4 g/t AuEq.

There’s currently more gold in Eskay Creek’s subsurface layers than was ever mined back in the day.

The average pit depth is 180 meters. It maxes out at 236 meters.

The current resource does NOT include results from a 2019, 14,000-meter drilling campaign designed to upgrade the resource and step out from known areas of mineralization.

Note the Inferred resource values (tonnes and grade) versus the Indicated resource values.

The Inferred grade is roughly 50% lower than the Indicated grade (3.0 g/t versus 5.9 g/t). The reason: where the drill holes in the Indicated areas of the deposit are spaced roughly 15 meters apart, the Inferred area drill holes are spaced between 50 to 100 meters apart. The further the distance between holes, the steeper the grade penalty. As the company infill drills the Inferred areas—zones where no historic mining took place—the grade stands to increase as the ounces shift into the higher confidence category.

This current 28k meter drilling campaign will go a long way towards pushing the Inferred material into the Indicated category. This will set the stage for a PFS.

Back in November of 2019, the company tabled a PEA with a fair bit of bulk:

An article I published earlier this year over at Tommy Humphreys ceo.ca offers a closer look at the company, and the deposit:

Skeena Resources (SKE.V) aggressively pushing Eskay Creek further along the development curve

Recent news

On April 23, Skeena dropped the following headline:

Skeena Intersects 4.11 g/t AuEq over 22.08 metres at Eskay Creek

With four rigs turning on a phase-one surface program, recent drilling focused on the 21B and 21C zones.

Phase one highlights:

- 3.62 g/t Au, 41 g/t Ag (4.11 g/t AuEq) over 22.08 m (SK-20-259) – 21B Zone

- 2.61 g/t Au, 10 g/t Ag (2.74 g/t AuEq) over 36.19 m (SK-20-263) – 21B Zone

- 3.91 g/t Au, 21 g/t Ag (4.18 g/t AuEq) over 19.60 m (SK-20-264) – 21B Zone

- 4.61 g/t Au, 203 g/t Ag (7.32 g/t AuEq) over 8.43 m (SK-20-248) – 21C Zone

According to the company…

“The 2020 Phase I infill program at Eskay Creek continues to demonstrate the excellent continuity of the current resource model which is derived largely from historical drilling. Phase I infill drilling within the 21B and 21C Zones, which are situated in the deeper portions and later phases of the planned open-pit mining sequence, have correlated extremely well with the historical drilling with respect to grades, widths and spatial distribution.”

When Skeena acquired Eskay Creek from Barrick back in 2017, it inherited over 700,000 meters of historic drill hole data. Recent drilling is successfully connecting the dots with those historic values:

“In the 21B Zone, historical drill hole C97853 (1997) positioned nearest to the current Phase I drilling intersected 3.07 g/t AuEq over 18.26 metres in rhyolite breccias and minor mudstones. This intercept is separated by a horizontal strike distance of 20 metres to the north, and the lithologies and grades are similar to those observed in 2020 infill drill holes with intercepts of 3.62 g/t Au, 41 g/t Ag (4.11 g/t AuEq) over 22.08 metres (SK-20-259) and 3.91 g/t Au, 21 g/t Ag (4.18 g/t AuEq) over 19.60 metres (SK-20-264). Additional thicknesses of mineralization were also intersected in SK-20-263 which averaged 2.61 g/t Au, 10 g/t Ag (2.74 g/t AuEq) over 36.19 metres. Precious metal mineralization hosted in this portion of the 21B Zone is largely associated with sericite altered rhyolite breccias and flows.”

The company is 4,327 meters into a planned 28,000 meter program.

Additional assays are pending.

The following video has Kelly Earle, Skeena’s VP of Communication, giving us a virtual tour of the Eskay Creek project.

Skeena also has a webinar scheduled for next Wednesday. I’ll be attending. To register, tap on the link below.

END

Greg Nolan

Disclaimer - Legal NoticeHighballerstocks.com (Greg Nolan) is not a licensed financial advisor and does not give investment advice.

The content of this report is for information purposes only.

Nothing contained herein should be construed as a recommendation or solicitation to buy or sell any security.

Always consult a licensed qualified investment advisor in your legal jurisdiction before making any investment decisions.

Though Highballerstocks.com (Greg Nolan) believes its sources to be credible, and the statements contained herein to be true, readers must conduct their own thorough due diligence, and or consult with a qualified investment advisor before important investment decisions are made.

Highballerstocks.com (Greg Nolan) accepts no responsibility or liability for the accuracy of the contents of this report.