With the junior exploration landscape constantly shifting—constantly evolving—this feels like an opportune time to lay out my current thinking and the projects I’m backing with capital.

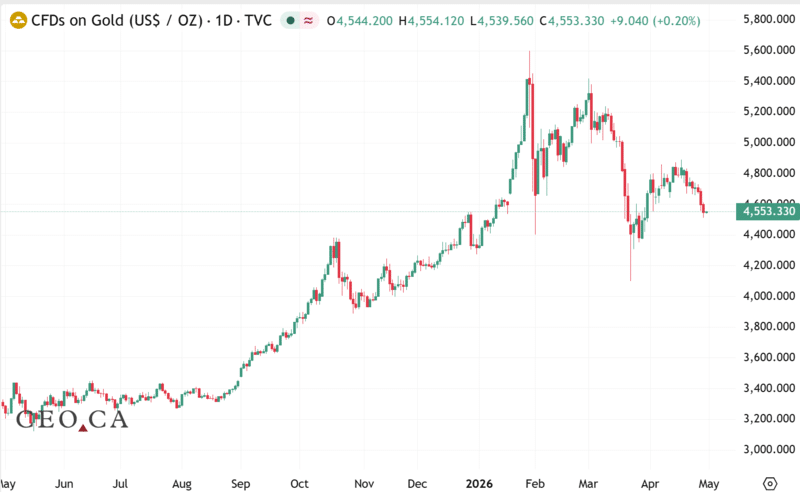

Precious metals remain volatile, but they’re consolidating comfortably above key support levels.

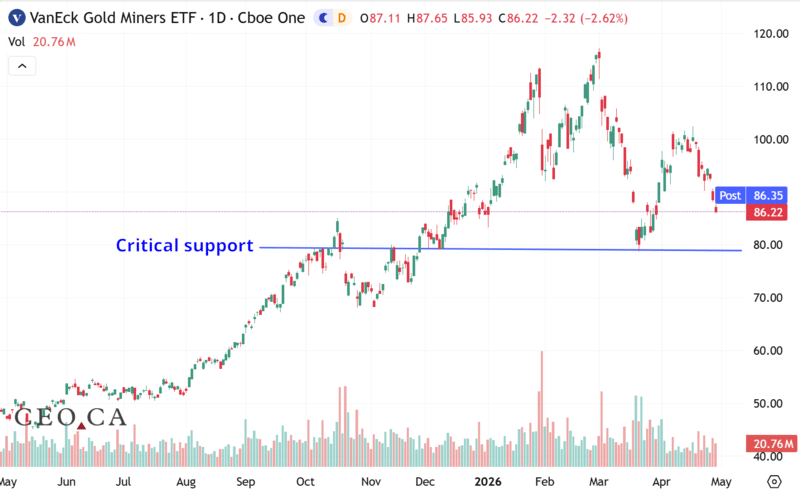

Senior equities are trading well off their highs, but they survived a test of critical support roughly five weeks ago. A one‑year GDX…

Meanwhile, on the junior exploration front, M&A activity is keeping things interesting for those of us positioned in the space.

The acquisition of Aurion, Rupert, and B2Gold’s interests in the Central Lapland Greenstone Belt of northern Finland by mining behemoth Agnico Eagle was a welcome exit for those of us with meaningful exposure to the region.

A one-year Aurion price chart…

In my July 2025 Highballer Report, I laid out my reasoning for owning Aurion when the stock was trading at $0.78:

Aurion’s Helmi Project shares a common boundary with Rupert’s Ikkari deposit (Helmi is a joint venture between Aurion—30% and B2Gold—70%). A part of Rupert’s deposit (and possibly a weighty swath of mineralization) runs onto Aurion’s JV claims. Rupert will need to acquire that chunk of ground before they can proceed with open pit development of Ikkari to minimize the negative (economic) impacts of a sub-optimal pit design.

I was wrong about who would ultimately make a move on Aurion, but I was right about the appeal of its flagship asset as a takeover target. – AGNICO EAGLE TO ACQUIRE AURION RESOURCES IN ALL-CASH TRANSACTION FOR APPROXIMATELY C$481 MILLION.

We’ve had a fair degree of success identifying potential takeover targets here at Highballer Central. Three additional companies we’ve tracked closely in these pages were also taken out by entities higher up the food chain over the past ten months. Northern Superior Resources was acquired by IAMGOLD at a very agreeable price—a solid multi‑bagger from the levels where we first began following it. Prime Mining was acquired by Torex Gold, and Orogen Royalties was acquired by Triple Flag Precious Metals (the SpinCo from that deal currently trades as Orogen Royalties Inc. under the symbol OGN.V).

Though I love a good grassroots exploration play—what boy doesn’t like a good treasure hunt?—my attention is drawn to plays that may appeal to a resource‑hungry predator: a mid‑ or senior‑tier producer.

M&A Poised to Accelerate?

Every day a mining company pulls ore out of the ground—every day they’re open for business—their mineral inventory shrinks. A robust pipeline of development projects is the key to long‑term survival in this business.

It wasn’t too long ago that producers were forced to scale back exploration spending and M&A activity due to a protracted, sector‑wide bear market. They couldn’t grow their mineral inventories organically or through acquisitions. But things have changed. In the wake of substantially higher precious metals prices, they’re now flush with cash, they’re resource‑hungry, and they’re in a spending mood. The Aurion–Rupert–B2Gold deal is a prime example of a trend that’s likely to gain momentum going forward.

If you’re a resource‑rich junior in a mining‑friendly jurisdiction, you’re vulnerable. And a predator may already have you in its sights.

Moving along…

Following the $481 million all‑cash takeout of Aurion, the real question becomes how to deploy the cash. As far as problems go, it’s a good one to have.

Rather than run through the 100‑plus junior entities I follow in the space, I’ll tell you what I’m nibbling at right now. And to be clear, none of this is advice. It’s simply fodder for your own due diligence.

Benz Mining (TSXV: BZ) – (ASX: BNZ)

- 333.86 million shares outstanding

- $674.39M market cap based on its recent $2.02 close

- Corp. pitch deck

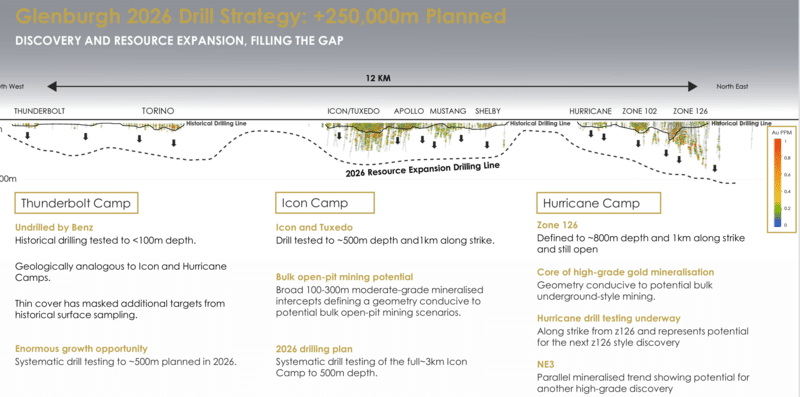

Benz is advancing multiple discoveries at its Glenburgh Gold Project in Western Australia, a district-scale belt with ~80 kilometers of strike at the northern margin of the Yilgarn Craton.

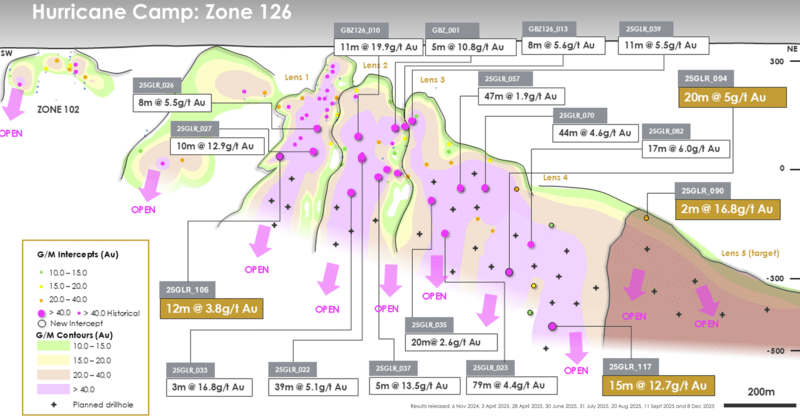

The company has divided Glenburgh into three distinct camps, each with its own geological character and two clear development pathways: thick, bulk‑style gold mineralisation (Icon–Apollo) and multiple high‑grade underground lenses (Zone 126).

A closer look at Zone 126, the high‑grade zone noted above and one of several lenses defined to date at Glenburgh.

There’s real conviction in play with this crew—a “special forces” geo‑team made up of ex‑AngloGold, Barrick, Sandfire, IGO, and Gold Road talent. With roughly A$94 million in the till following a recent A$75 million bought deal, Benz is targeting 250,000 meters of exploration and resource definition drilling at Glenburgh in 2026. Management believes the potential is wide open—and they may be right. An April 9 press release: Multiple New High-Grade Discoveries Drive Expansion at Hurricane Camp.

There’s more under the hood here: 170 kilometers to the east of Glenburgh, at the company’s Mt Egerton Gold Project, recent drilling tagged a new high-grade discovery beneath the historic Hibernian Gold Mine – Benz Announces New Ultra High Grade Gold Discovery at Mt Egerton.

Highlights from this March 16 press release:

- New ultra-high grade Kilkenny discovery offset beneath the historic Hibernian Gold Mine validates Benz structural model.

– 7 meters at 223 g/t gold from 270 meters within 11 meters at 144 g/t gold; - High-grade satellite opportunity for Glenburgh – Mt Egerton located ~170 kilometers from the Glenburgh Gold Project with potential to provide additional high-grade satellite ore. Previous intercepts from Hibernian include:

– 9 meters at 107 g/t gold;

– 5 meters at 96 g/t gold;

– 4 meters at 92 g/t gold.

Benz isn’t exactly cheap, but there may be multiple layers of upside embedded in these subsurface horizons. Continued success at the business end of the drill bit could put this one squarely in the crosshairs of a resource‑hungry predator.

Kenorland Minerals (TSXV: KLD) – (OTC: KLDCF)

- 79.94 million shares outstanding

- $171.88M market cap based on its recent $2.15 close

- Corp Presentation

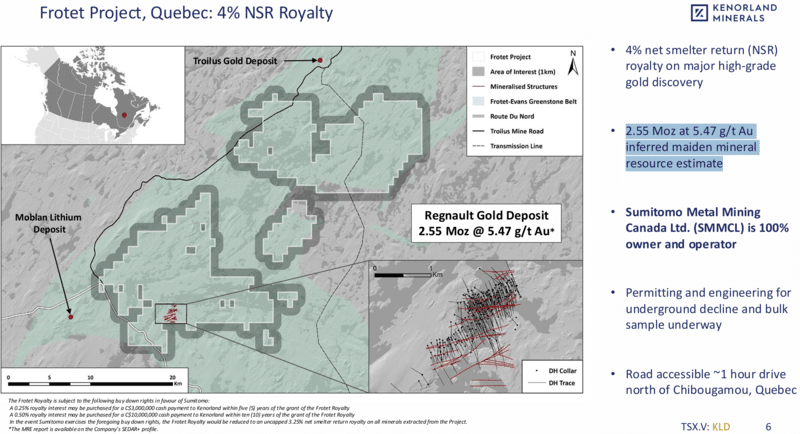

Kenorland is a well run, tightly structured hybrid prospect generator boasting roughly C$16,265,000 in working capital, $18,250,000 in equity interests (including private holdings), a highly prospective portfolio of projects with strategic JV’s, and a fat 4% NSR on the high-grade Frotet orogenic gold system.

Sumitomo Metal Mining Canada now owns 100% of Frotet, but Kenorland’s 4% NSR covers an Inferred resource base that currently stands at 2.55 million ozs grading 5.47 g/t Au in a structure that remains open at depth and along strike. Numerous high-grade intercepts outside the current geological model underscore the immediate resource expansion and exploration upside.

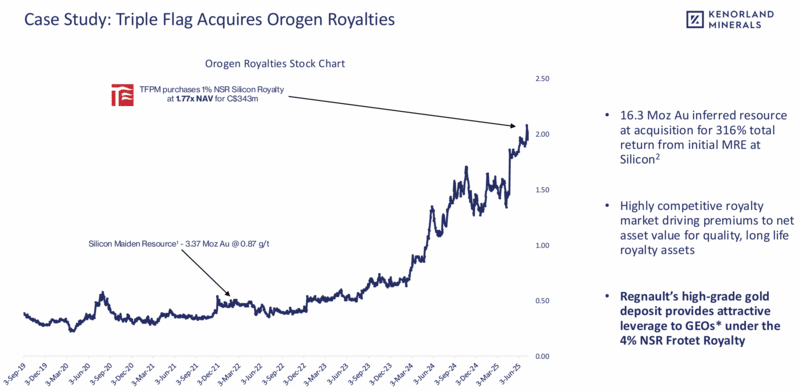

Part of the appeal in owning Kenorland as a core holding is that someday, a royalty‑hungry entity could come knocking, wanting the Frotet NSR in their portfolio—fully aware that these high‑grade orogenic deposits tend to grow… often dramatically so.

To demonstrate the potential, the Triple Flag acquisition of Orogen Royalties—a company we followed closely in these pages—is highlighted in Kenorland’s pitch deck as a case study. This is one of the reasons I’m here.

There are multiple potential catalysts here, including the South Uchi Project in the prolific Red lake mining camp of Ontario. South Uchi is optioned to newly listed Auranova Resources (TSXV: AURA). The JV carries Kenorland to the PEA stage at 30% and secures a 2% uncapped NSR. The partners are hunting for a Great Bear–style discovery.

An April 28 press release – Kenorland Minerals and Auranova Resources Announce Completion of Spring Drill Program at the South Uchi Project, Ontario.

Their JV with Centerra Gold (TSX: CG) includes the Western Wabigoon and Flora projects, where Kenorland is carried to the pre‑feasibility stage at 30% and holds a 2% NSR on each. A 5,000‑meter drill campaign is slated for Western Wabigoon in 2026.

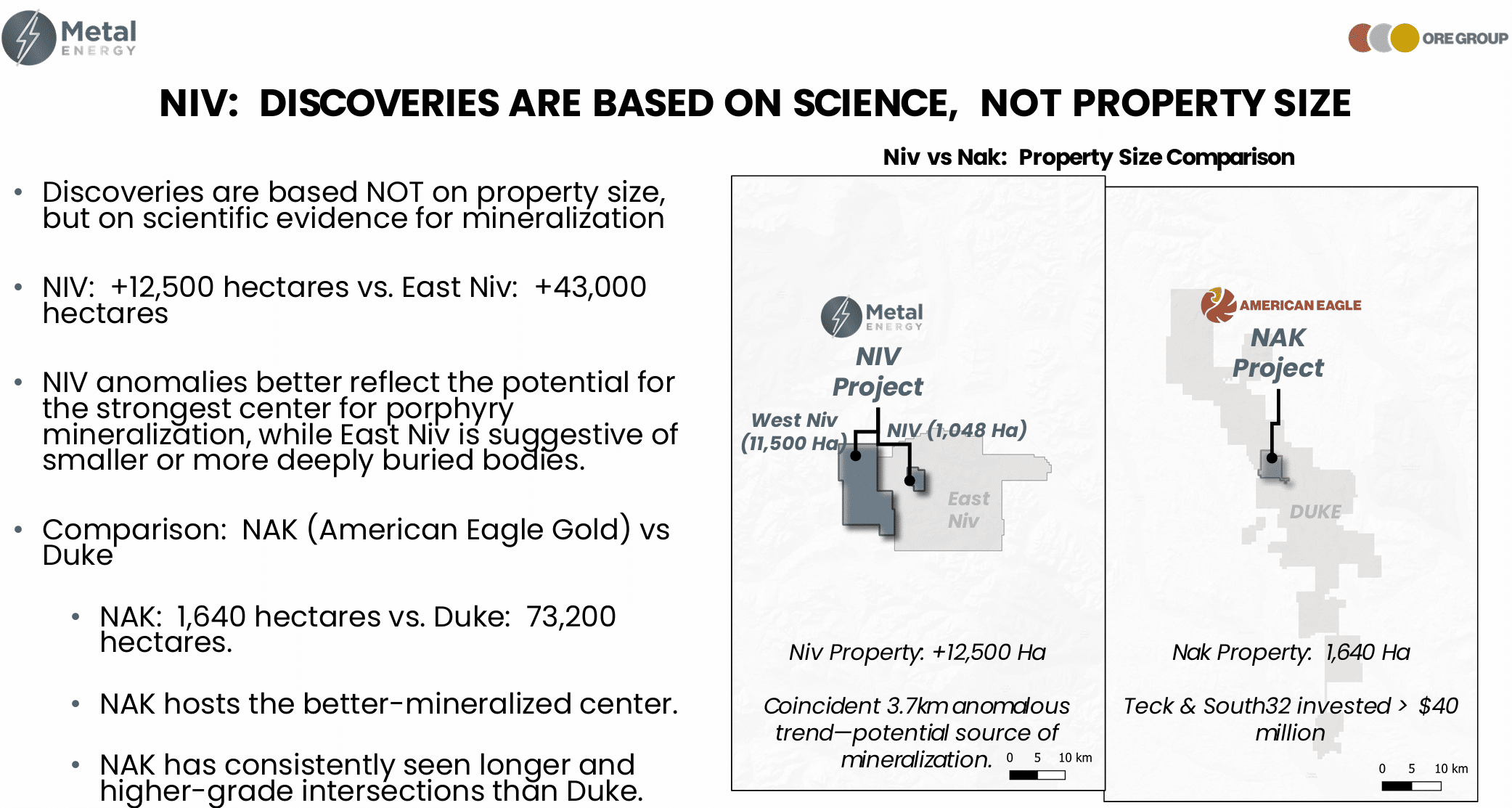

Metal Energy Corp (TSXV: MERG) – (OTC: MEEEF)

- 45.2 million shares outstanding

- $39.78M market cap based on its recent $0.88 close

- Corp pitch deck

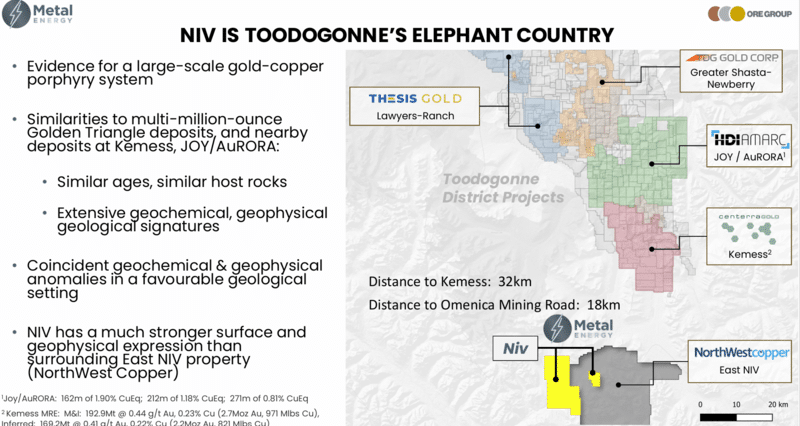

I discovered this one while scouring the Toodoggone district of central British Columbia for well‑run companies with geologically prospective land positions—companies with similar host rocks as nearby multi‑million‑ounce deposits such as Kemess, Lawyers, AuRORA, and Shasta—and with plans to mobilize a drill rig or two once winter loosens its grip. According to the company’s website, their flagship NIV Project represents the best undrilled gold-copper porphyry target in BC .

I like the discovery potential here—the “treasure hunt” intrigue of the play. I also like management and the tight share structure. And I like the fact that Centerra and Teck have each taken a 9.9% equity interest in the company.

Adding to the appeal, Northwest Copper (TSXV: NWST) drilled a discovery less than two kilometers east of MERG’s property boundary: 0.56% CuEq over 81.6 meters, including 1.02% CuEq over 14.8 meters.

The company dropped a press release earlier today concerning the upcoming drill program – Metal Energy Announces Drill Program at NIV.

Highlights:

- First-ever drilling at NIV will total 6,000 meters across 12 holes;

- Drilling will test a compelling 5 km long gold-copper-silver-molybdenum soil anomaly coincident with a multi-parameter geophysical signature characteristic of porphyry systems;

- Host rocks correlate in age with those at the nearby Kemess deposit and across BC arc terranes, including the Golden Triangle;

- Mobilization is targeted for June.

This one might warrant a closer look, especially with its tight structure. If they hit what they suspect is lurking in NIV’s subsurface, the discovery could trigger a meaningful re-rating.

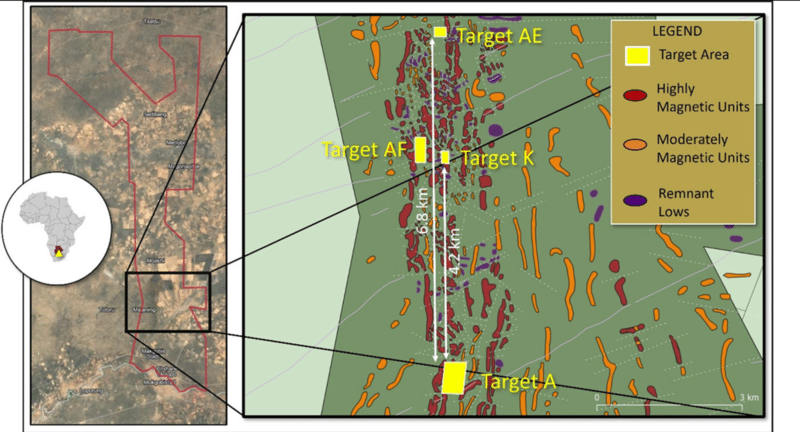

North Arrow Minerals (TSXV: NAR)

- 45.99 million shares outstanding

- $12.88M market cap based on its recent $0.28 close

- Corp presentation

Last November, the company reported a discovery at Kraaipan with an RC intercept of 1.56 g/t Au over 30 meters, including 7.32 g/t Au over 3 meters from surface, plus 4.26 g/t Au over 4 meters from 10 meters depth. Quoting the November 4 press release: This discovery caps the successful completion of a US$1 million regional reconnaissance program that has identified six priority gold targets across 45 km of the underexplored Kraaipan Greenstone Belt.

On April 16 (two weeks back), the company updated its exploration efforts at Kraaipan—a combination of geochem (surface sampling), geophysics, and two phases of drilling – North Arrow Extends Mineralized Footprint at Kraaipan Gold Project, Botswana.

Drilling-related highlights from the guts of this April 16 release:

Rotation 1 Drilling Complete – Target A

- 20 RC holes totaling 1,103m completed, testing four high-priority grids along an interpreted ~700m NE–SW strike length.

- Field logging of chips confirms quartz veining, weathered sulphides and a host-rock assemblage consistent with the same geological setting that delivered the flagship 2025 RC intercept of 30m @ 1.56 g/t Au (hole KR25-157) at Target A.

- Assay results expected in Q2 2026.

Rotation 2 Drilling Commenced – Targets AE and AF

- 20 holes / ~1,100m planned, designed to test strike extensions at Target AE and to increase confidence in the 450m trend at Target AF.

- Scheduled for completion in early May 2026.

Like MERG, the company’s tight structure could set the stage for dramatic share‑price trajectory should the RC assays come back positive.

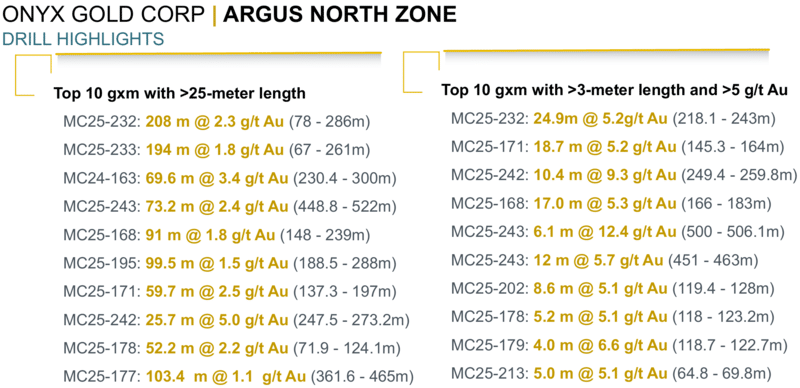

Onyx Gold (TSXV: ONYX) – (OTC: ONXGF)

- 85.59 million shares outstanding

- $100.99M market cap based on its recent $1.18 close

- Corp pitch deck

Onyx, a spinout from HighGold Mining (taken out by Contango in early May, 2024), started out as a cheap, tightly structured junior with an interesting suite of properties in the prolific Timmins camp along the Abitibi Greenstone Belt. To the delight of loyal shareholders, the company reported a solid hit from the Argus North Zone at its flagship Munro-Croesus Project less than a year later- Onyx Gold Intersects 3.4 g/t Gold Over 69.6 Meters Including 5.4 g/t Gold over 34.5 Meters at Munro-Croesus Project and Announces Option Agreement.

The values highlighted in the text of the above headline included high-grade subintervals of 13.9 g/t gold over 9.5 meters and 38.5 g/t gold over 3.0 meters.

The company has been reporting a steady stream of decent values from Munro-Croesus ever since. The most recent assays dropped on March 31, this time highlighting the Argus Main Zone – New High-Grade Structure at Argus Main: 4.9 g/t Gold over 15.0 Meters Within 1.3 g/t Gold over 77.2 Meters; 2.9 g/t Gold over 12.5 Meters Within 1.2 g/t Gold over 99.5 Meters.

A snapshot of some of the more impressive intercepts drilled to date at Argus North (slide 13 from the company’s pitch deck)…

The drill campaign at Munro‑Croesus has recently been expanded to 110,000 meters as the company pushes to establish district‑scale potential—60,000 meters remain to be drilled through year‑end. Four rigs are currently turning at the project, setting the stage for robust news flow through the balance of 2026. The 110,000‑meter program is fully funded, and the company has roughly $22 million in the treasury.

The share structure is still reasonably tight on this one, an increasingly rare phenomenon in this Wild West arena.

Finally, briefly…

Gold Royalty Corp (NYSE: GROY)

- 175.39 million shares outstanding

- $591.08M market cap based on its recent $3.37 close

- Corp presentation

GROY holds a diversified portfolio of over 240 royalties and streams on projects throughout the Americas, many of which are either cash‑flowing or in the development phase. Included in the mix is a 2.0% to 3.0% NSR on on Agnico Eagle’s Canadian Malartic Project.

On April 27, GROY dropped Q1 earnings – Gold Royalty Announces Record First Quarter 2026 Preliminary Results.

Preliminary Q1 results:

In the first quarter of 2026, the Company achieved record Total Revenue, Land Agreement Proceeds and Interest* of $9.4 million and record revenue of $7.2 million. Total Revenue, Land Agreement Proceeds and Interest* equates to 1,920 gold equivalent ounces (“GEOs”)* in the first quarter, a 162% increase relative to the same period last year, and an increase of almost 80% from the previous quarter.

Gold Royalty maintains its 2026 full-year production guidance of 7,500 – 9,300 GEOs as released on March 18, 2026, with production more heavily weighted to the second half as DPM Metals’ Vareš mine production is expected to reach its full run rate of 850,000 tonnes per year in 2026 and as Fortitude Gold’s County Line mine ramps up after commencing operations in January.

I view GROY as a potential takeover candidate for an entity higher up the royalty food chain looking to broaden its asset base.

Companies on my radar, but not yet in the portfolio

Mayfair Gold (MFG.V) – (MINE.NYSE)

- 67.08 million shares outstanding

- $264.97M market cap based on its recent $3.95 close

- Corp presentation

Prospector Metals (PPP.V) – (PMCOF.OTC)

- 157.02 million shares outstanding

- $227.68M market cap based on its recent $1.45 close

- Corp presentation

Radisson Mining (RDS.V) – (RMRDF.OTC)

- 434.04 million shares outstanding

- $442.72M market cap based on its recent $1.02 close

- Corp Pitch deck

— END

Greg Nolan

Full disclosure: The author has no business relationship with any company mentioned in this report. In terms of stock ownership, the author holds positions in Benz Mining (TSXV: BZ), Gold Royalty Corp warrants (NYSE: GROY.WS), Kenorland Minerals (TSXV: KLD), Metal Energy Corp (TSXV: MERG), North Arrow Minerals (TSXV: NAR), and Onyx Gold (TSXV: ONYX). Consider the author extremely biased with respect to these holdings. The author also reserves the right to buy or sell any of the above entities at any time, without notice.

Disclaimer - Legal NoticeHighballerstocks.com (Greg Nolan) is not a licensed financial advisor and does not give investment advice.

The content of this report is for information purposes only.

Nothing contained herein should be construed as a recommendation or solicitation to buy or sell any security.

Always consult a licensed qualified investment advisor in your legal jurisdiction before making any investment decisions.

Though Highballerstocks.com (Greg Nolan) believes its sources to be credible, and the statements contained herein to be true, readers must conduct their own thorough due diligence, and or consult with a qualified investment advisor before important investment decisions are made.

Highballerstocks.com (Greg Nolan) accepts no responsibility or liability for the accuracy of the contents of this report.