Last week gave us what we were looking for—significant upside price trajectory in the Highballer portfolio (Pure Gold, HighGold, Coral Gold, and White Gold).

We have both movers and news-makers to report. We’ll start at the top of the alphabet and move on down.

Cartier Resources (ECR.V) – (ECRFF.OTC)

On May 13, our deep value development play tabled news that it had resumed drilling at its Chimo Mine project in the Val-d’Or mining camp.

read: Cartier Resumes Drilling on the Chimo Mine Property

Drilling continues with two rigs focusing on extending known mineralization at depth.

According to the press release:

Zones 5B4-5M4-5NE and 5CE, situated 450 m east of the underground infrastructures are being drilled reported excellent results in 2020 over a distance of 550 m below known zones. This cluster of gold-bearing zones extends from surface to a depth of 1,300 m and now include the new Zone 5CE. As well, internal engineering studies and tests of industrial sorting of the mineralisation are in progress in order to assess possibilities of cost reduction while increasing gold ounce recuperation, which in turn could contribute to increasing the mineral resource of the property. The first internal engineering study was completed with positive conclusions.

For those unfamiliar with the Cartier story, total gold resources at its Central, North and South Corridors contain:

- 4,017,600 tonnes at an average grade of 4.53 g/t Au for a total of 585,190 ounces gold in the Indicated category;

- 4,877,900 tonnes at an average grade of 3.82 g/t Au for a total of 597,800 ounces gold in the Inferred category.

The ounce count at Chimo now stands at 1,182,990. And I suspect there’s more to come.

Aside from Chimo, on deck is a robust pipeline of brownfield projects the company shrewdly acquired for pennies on the dollar—Benoist, Wilson, and Fenton.

Cartier’s share price has been stair-stepping higher since the mid-March liquidity event and could be setting up for an assault on higher ground—its 52-week highs in the $0.20 range.

Cartier is a company with endgame potential (it may be in the crosshairs of a resource-hungry Producer).

Coral Gold (CLH.V) – (CLHRF.OTC)

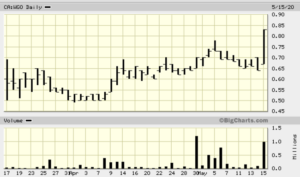

On NO news, save for its undervalued status, Coral took out multi-year highs in recent sessions. The chart below is a five-year weekly view of the company’s common shares:

The following chart, an up-close 3-month daily view, homes in the company’s recent push to higher ground:

Coral Gold, like Cartier Resources above and Defense Metals below, was elevated to top-shelf status in my maiden Highballer piece earlier this year.

Coral holds an uncapped sliding scale 1% to 2.25% NSR on over 2.7 million ounces at Barrick Gold’s Robertson Property located along the prolific Cortez Gold Trend of northern Nevada.

Robertson is a joint venture between Barrick (61.5%) and Newmont-Goldcorp (38.5%). This JV among mining behemoths is called Nevada Gold Mines—NGM for short.

It’s important to note that Robertson’s ounces are now considered part of the mineral resource base for the Cortes Mine Complex.

It’s also important to note that finding a deep, rich ‘feeder’ type deposit is a high-priority for NGM. Such a discovery could blow this play wide open.

My maiden report on this tightly held, tightly structured company should help bring you up to speed on this compelling royalty play in the heart of the Cortes Trend:

read: Highballer’s Top Three Picks for 2020

Defense Metals (DEFN.V) – (DFMTF.OTC)

I covered the recent news out of the Defense Metals camp in a fair bit of detail last Friday over on Chris Parry’s Equity Guru.

Last Friday’s news added significantly greater depth to the Defense Metals story—a development the market failed to grasp.

This lack of appreciation may represent an opportunity for those not yet positioned in this rapidly evolving REE play, one of the better values I see in the junior exploration arena.

The news…

read: Defense Metals Announces Updated and Increased Mineral Resource Estimate for Its Wicheeda Rare Earth Element Carbonatite Deposit

The highlights:

- A 49% increase in overall tonnage (1) based on the results of the 2019 diamond drilling of 13 holes totaling 2,005 meters;

- A 30% increase in overall average grade (1), in part through the incorporation of potentially economically significant praseodymium not previously estimated;

- Conversion of 4,890,000 tonnes to Indicated category (1) previously defined as Inferred;

- Increased Inferred Resources by 730,000 tonnes in comparison to the initial Wicheeda MRE1;

- Potential for expansion of the Wicheeda Deposit to the north and west in the down plunge direction.

This updated 43-101 comprises an Indicated Mineral Resource of 4,890,000 tonnes averaging 3.02% LREO (Light Rare Earth Elements), in addition to an Inferred Mineral Resource of 12,100,000 tonnes averaging 2.52% LREE, reported at a cut-off grade of 1.5% LREE (sum of cerium (Ce), lanthanum (La), neodymium (Nd), praseodymium (Pr), and samarium (Sm); in addition to niobium (Nb) percentages).

There exists a strategic component to this near-surface, high-grade, open-pittable REE resource, one that adds tremendous depth to the story.

As emphasized in Friday’s Equity Guru piece, “tensions between the U.S. and China are high. With China in control of the Rare Earth refining market and the U.S. pushing to source and secure domestic supply, Wicheeda’s strategic importance can’t be overstated. In fact, the company is currently being reviewed by the US Department of Defense to become a preferred vendor under the Defense Production Act Title III program.”

The next catalysts for the company include:

- A diamond drilling campaign designed to follow-up on significant mineralization encountered to the north, and to the west (and at depth) of the current resource;

- The processing of its 30-tonne Wicheeda bulk sample in a pilot plant environment to confirm metallurgy, and produce a large volume of concentrate for downstream hydrometallurgy testing.

- The initiation of baseline environmental studies;

- A first pass economic study (a PEA);

- Entering into discussions re MOUs (memorandums of understanding) and potential offtake agreements.

Is the market myopic, suffering from a complete lack of foresight or intellectual insight?

Good question.

The market appeared to be onto some earlier last week when the shares went on a tear, tagging levels we hadn’t seen in nearly a year. But the gains were disappointingly short-lived.

I suspect it’s only a matter of time before the market truly wakes up to the strategic and economic potential of this stock.

HighGold Mining (HIGH.V) – (HGGOF.OTC)

HighGold’s Johnson Tract (JT) deposit is one of the more compelling exploration/development plays I’ve come across in the junior arena. Clearly, JT has Tier One potential.

A maiden resource estimate reported on April 29 continues to play well for a market in search of A-List opportunities… of which there is only a handful, in my estimation.

Resource highlights:

- Indicated Resource of 2.14 million tonnes (“Mt”) grading 10.93 grams per tonne (“g/t”) gold equivalent (“AuEq”) for 750,000 ounces AuEq;

- Additional Inferred Resource of 0.58 Mt grading 7.16 g/t AuEq for 134,000 ounces AuEq;

- The deposit includes a high-grade core of 1.25 Mt Indicated grading 14.54 g/t AuEq for 583,000 ounces AuEq at an 8 g/t AuEq cutoff;

79% of total resource tonnage in the Indicated category, including 85% of the total AuEq ounces; - Steeply dipping deposit with typical horizontal thickness of 25 to 50 meters, strike length of 300 meters and excellent continuity of grade from surface to a depth of 275 meters;

- Resource open to expansion and multiple high-priority targets located nearby, including the prime Northeast Offset target that is believed to be the fault-displaced continuation of the JT Deposit (editors note: this offset target really gets the speculative juices flowing);

- High metal recoveries and concentrates low in deleterious elements are predicted based on past metallurgical test work, including forecasted total gold recovery of up to 96%.

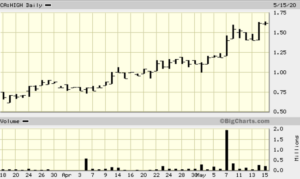

Last weeks price action in the stock was a welcome and merited event (note the volume surge on May 7):

My maiden HighGold article from late January 2020 should help answer your questions if you’re wondering what all the fuss is about:

read: A high-grade gold and base metal play with Tier-1 potential – HighGold Mining (HIGH.V)

Pure Gold (PGM.V) – (LRTNF.OTC)

On May 11, Pure Gold updated shareholders re progress at its PureGold Mine project in the Red Lake mining district of Ontario (Red Lake is known as the high-grade gold capital of the world).

read: Canada’s Next Gold Mine on Track for First Gold Pour in Q4

The company is on schedule for its first gold pour by years end.

Referring to the rising gold price environment we currently find ourselves in—gold is trading north of $1,170 overseas as I type—the company stated:

Current market conditions improve our $CDN/oz gold price by 41% from the base case. Base-case parameters for our 2019 feasibility are US$1,275 per ounce of gold and a U.S. to Canadian exchange rate of $1.33, equal to a CDN $1,700 gold price. As a Canadian gold producer, the combination of stronger gold price and declining Canadian dollar has a material positive impact. As at May 7th, 2020, with gold at CDN$2,400 per ounce, the mine would generate an additional C$679 million in revenue over the base case.

The Feasibility Study:

- Probable Mineral Reserves of 3.5 Mt at 9.0 g/t containing 1.0 million ounces of gold;

Low initial capital requirement of $95 million including a 9% contingency; - Mine life of 12.2 years with a 13 month pre-production period;

- Peak annual production of approximately 125,000 ounces with average annual gold production in years 3 through 7 of approximately 102,000 ounces;

- Life of mine (LOM) direct operating cash cost estimated at US$607 per ounce of gold recovered;

- LOM all in sustaining cash cost estimated at US$787 per ounce of gold recovered;

Pre-tax NPV5% and IRR of $353 million and 43% respectively with a 3.0 year payback of initial capital; - After-tax NPV5% and IRR of $247 million and 36% respectively with a 3.4 year payback of initial capital.

The market took this as its cue to accumulate shares in this highly leveraged, soon-to-be-producing company… not to mention its 47 square kilometers of highly prospective terra firma.

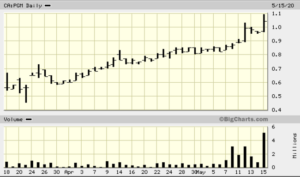

The above chart—a two month daily—captures last week’s dramatic price/volume action.

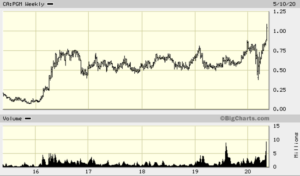

This next chart—a five year weekly—demonstrates PGM’s multi-year breakout. There’s an old saying in TA circles that goes something like, “the longer the base, the higher in space”. This is a nice long base PGM is breaking out from (the same goes for Coral Gold further up the page)…

Greater insights into this Red Lake success story can be gained via my maiden PGM article six weeks back (the share price at the time was $0.64):

read: Pure Gold Mining (PGM.V) – a high-grade Red Lake development story

White Gold (WGO.V) – (WHGOF.OTC)

Last week, we noted:

One of the companies on my shortlist—White Gold (WGO.V)—hasn’t produced much in the way of news in recent weeks. As a consequence, its share price remains mired in the lower end of its 52-week range, waiting for a catalyst to trigger a push to higher ground.

Current prices may represent a low risk entry point.

On Friday, May 15, we received the catalyst we were looking for when the company dropped the following headline…

read: White Gold Corp. Announces Fully Subscribed C$6 Million Private Placement of Flow-Through Common Shares; Agnico Eagle and Kinross to Maintain Interest; Eric Sprott to Participate

The market, after digesting the significance of the raise early in Friday’s session, took off and didn’t look back (note the spike in price AND volume).

Noteworthy, in the guts of this press release:

“Pursuant to the Investor Rights Agreement between the Company and Agnico Eagle Mines Limited (TSX: AEM) dated December 13, 2016, Agnico has indicated that it intends to maintain its 17.1% interest in the Company. Additionally, pursuant to the Investor Rights Agreement between the Company and Kinross Gold Corporation (TSX: K) dated June 14, 2017, Kinross has indicated that it intends to maintain its 17.1% interest in the Company.”

Adding an additional vote of confidence to this asset-rich Yukon ExploreCo is the participation of Eric Sprott, wading in for a piece of the action.

The two mining giants, and the Canadian billionaire, know a good value when they see it.

David D’Onofrio, White Gold CEO:

“We are very grateful for the continued support of our major shareholders and excited to welcome Eric Sprott as a new shareholder. We look forward to commencing our 2020 field season where we will follow up on some exciting new discoveries and look to continue to increase our existing mineral resources. We are finalizing the details of our 2020 work campaign which is expected to be announced in the coming weeks” .

According to the rules, these flow through funds need to go directly into the ground.

This upcoming work program, expected to include significant follow-up drilling on new discoveries tagged during the 2019 field season, should generate substantial newsflow over the coming months.

For those unfamiliar with the company and its land dominant land position in the White Gold district, my maiden Highballer coverage should bring you up to speed:

read: White Gold – unparalleled discovery potential in Canada’s Yukon

Also…

read: Deep value in the Highballer portfolio – Cartier (ECR), Defense (DEFN.V), and White Gold (WGO.V)

I’ll be looking for some follow-through price action when the market opens tomorrow in Canada, May 19th.

Final thought

The recent across-the-board price action of late suggests it’s game on for the junior exploration arena. And it’s about time. It’s been a long enough wait.

END

—Greg Nolan

Disclaimer - Legal NoticeHighballerstocks.com (Greg Nolan) is not a licensed financial advisor and does not give investment advice.

The content of this report is for information purposes only.

Nothing contained herein should be construed as a recommendation or solicitation to buy or sell any security.

Always consult a licensed qualified investment advisor in your legal jurisdiction before making any investment decisions.

Though Highballerstocks.com (Greg Nolan) believes its sources to be credible, and the statements contained herein to be true, readers must conduct their own thorough due diligence, and or consult with a qualified investment advisor before important investment decisions are made.

Highballerstocks.com (Greg Nolan) accepts no responsibility or liability for the accuracy of the contents of this report.

Your weekly letter is short and direct…….perfect.

Appreciate that Stephan.